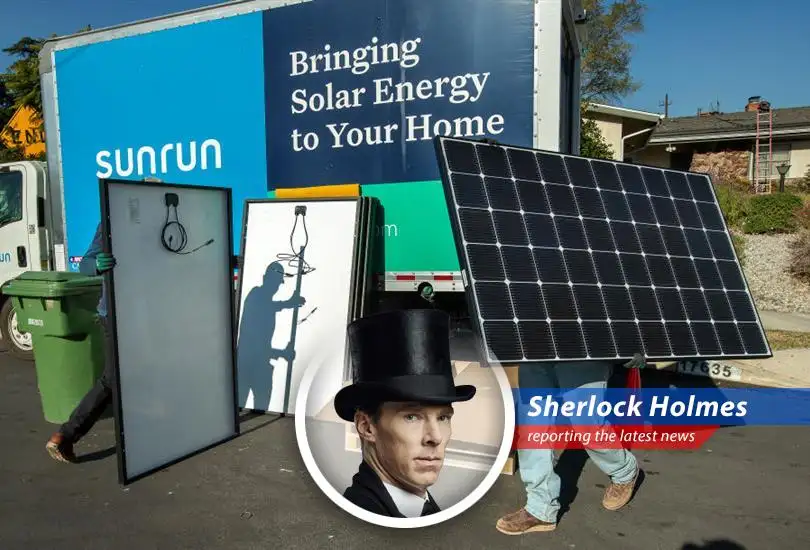

The Curious Case of the Plummeting Solar Stock

The game is afoot my dear readers and this time it involves the rather turbulent world of solar energy. RBC Capital Markets it seems has developed a rather pessimistic outlook on Sunrun (RUN) a company that once shone so brightly. The analyst a Mr. Christopher Dendrinos has downgraded the stock to 'sector perform' from 'outperform'. One might say the sun has set on their previous assessment. As I always say data data data! I can’t make bricks without clay!

A Seven Dollar Deduction: A Study in Scarlet (Figures)

The price target slashed by a considerable $7 now sits at a paltry $5. This according to my calculations represents a potential downside of 13.5% from Tuesday's close. A rather elementary deduction wouldn't you agree Watson? But as I have repeatedly mentioned in my cases it has long been an axiom of mine that the little things are infinitely the most important.

The Senate's Shadow: A Scandal in Bohemia (Bill)

The root of this misfortune it appears lies in the U.S. Senate's reconciliation bill. This piece of legislation has cast a long shadow over solar stocks causing a veritable cratering on Tuesday. Sunrun in particular suffered a catastrophic plunge of approximately 40% marking its worst single day loss on record. A clear indication that the political winds are shifting or as I would say 'There is nothing more deceptive than an obvious fact.'

Taxing Times: The Sign of Four (Credits)

The bill's language it seems threatens the elimination of tax credits for residential solar leasing. While Mr. Dendrinos points out that a substantial 70% of Sunrun's customer base is involved in storage which should retain its credits the overall picture remains murky. This uncertainty my dear Watson is the very air a cunning criminal—or in this case a struggling solar company—breathes. I would not trust it to advise me to the time of day.

Cash Generation Conundrum: The Hound of the Baskervilles (Financials)

The analyst also suggests that this environment makes it exceedingly difficult for Sunrun to achieve positive cash generation particularly given the industry's current cost structure. He estimates that residential solar costs would need to be significantly lower—10% to 20% below current utility rates—to entice customers. A rather ambitious perhaps even impossible feat. One begins to suspect foul play or at least poor planning! The world is full of obvious things which nobody by any chance ever observes.

Austerity Measures and Uncertain Futures: The Final Problem (Maybe?)

In conclusion while Mr. Dendrinos believes that Sunrun's scale and market position may allow it to compete the path back to positive cash generation remains uncertain. The industry's long term cost structure and demand are equally unclear. In the meantime Sunrun shares continue to struggle facing their fifth consecutive losing year. As I always say 'You see but you do not observe.' One must dig deeper Watson to truly understand the mysteries of the market! It has long been an axiom of mine that the little things are infinitely the most important.

Sunrun solar energy stock downgrade RBC Capital Markets tax credits financial analysis market trends investment renewable energy economic forecast

Comments

- No comments yet. Become a member to post your comments.

From Sherlock Holmes

Breaking News

All Rights Reserved © 2023